Architects play a crucial role in shaping the built environment, but their work also comes with substantial risks. One of the most effective ways to extenuate these risks is through Architect Professional Liability Insurance. This type of policy provides coverage for architects against claims of negligence, errors, and omissions that may arise from their professional services. Understanding the importance and benefits of this insurance is essential for any architect looking to protect their practice and reputation.

Understanding Architect Professional Liability Insurance

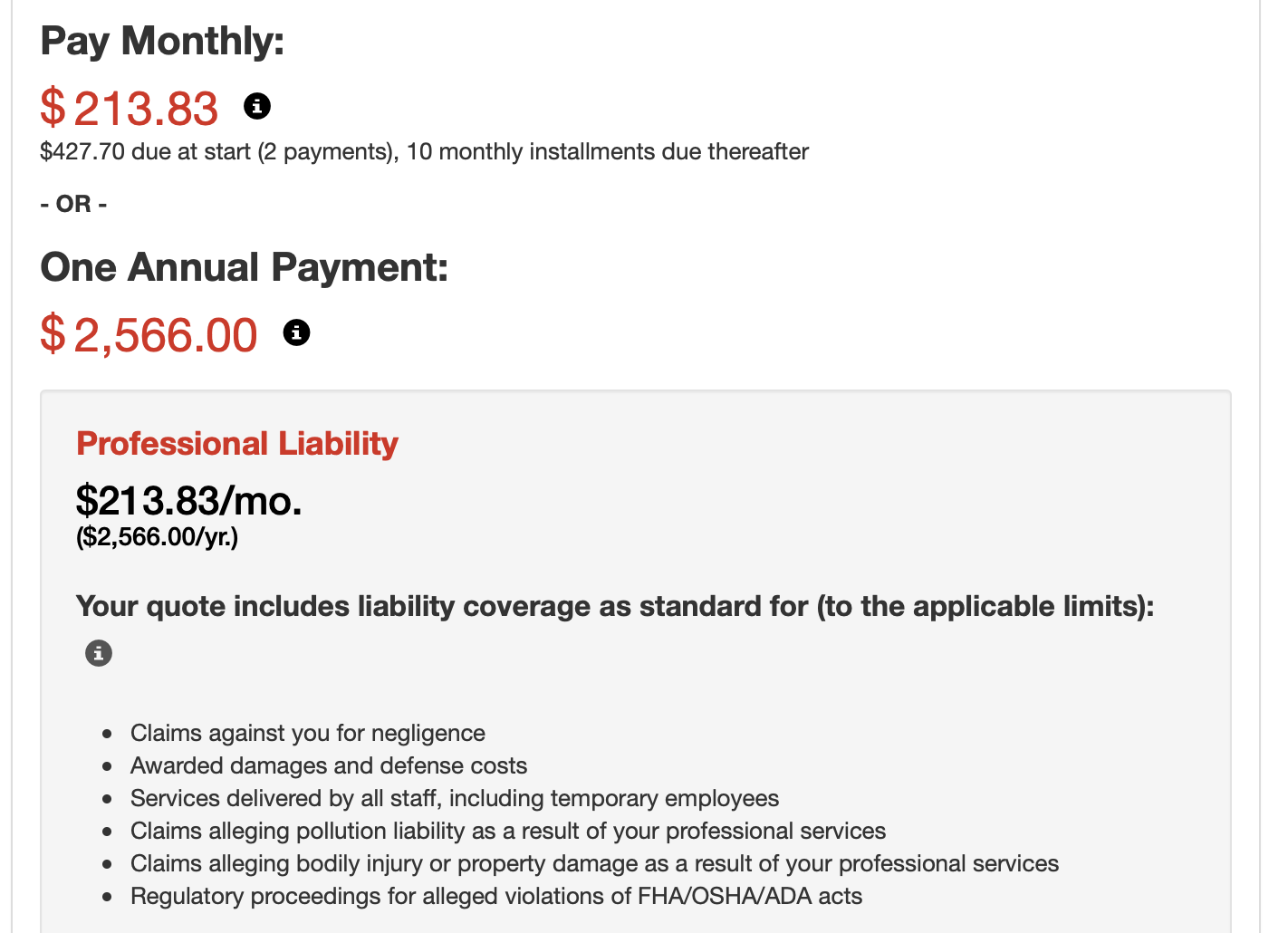

Architect Professional Liability Insurance, also known as Errors and Omissions (E O) policy, is contrive to protect architects from financial losses lead from claims of professional negligence. These claims can arise from various situations, such as design flaws, building delays, or failures in project management. The policy covers legal defense costs, settlements, and judgments, ascertain that architects can proceed their practice without the fiscal burden of such claims.

Key Benefits of Architect Professional Liability Insurance

There are several key benefits to obtaining Architect Professional Liability Insurance:

- Financial Protection: The indemnity covers the costs associated with legal defense, settlements, and judgments, protect the architect's personal and business assets.

- Reputation Management: By feature policy, architects can present their commitment to professionalism and obligation, which can raise their report in the industry.

- Peace of Mind: Knowing that they are protected against potential claims allows architects to focus on their act without never-ending worry about legal issues.

- Client Confidence: Many clients require architects to have Architect Professional Liability Insurance as a stipulation of contract, ascertain that they are protect in case of any issues.

Types of Coverage

Architect Professional Liability Insurance can be tailored to converge the specific needs of an architect's practice. The types of coverage typically include:

- Claims Made Policy: This type of policy covers claims made during the policy period, regardless of when the alleged error or omission occurred. notably that coverage may be set if the policy is not renew.

- Occurrence Policy: This policy covers claims arise from incidents that happen during the policy period, even if the claim is made after the policy has die. This type of coverage is oft more comprehensive but can be more expensive.

- Extended Reporting Period (ERP): Also known as a "tail", this coverage extends the reporting period for claims made policies, permit architects to report claims after the policy has choke.

Factors Affecting Premiums

The cost of Architect Professional Liability Insurance can vary based on several factors. Understanding these factors can assist architects get inform decisions when selecting a policy:

- Size of the Firm: Larger firms with more employees and higher revenue may face higher premiums due to increase risk exposure.

- Type of Projects: The complexity and risk assort with the types of projects an architect undertakes can touch premiums. High risk projects, such as those regard hazardous materials or complex engineering, may consequence in higher costs.

- Claims History: A history of claims can increase premiums, as insurers view the architect as a higher risk.

- Coverage Limits: Higher coverage limits will result in higher premiums, but they also render greater protection against possible claims.

- Deductibles: Choosing a higher deductible can lower premiums, but it also means the architect will pay more out of pocket in the event of a claim.

Choosing the Right Policy

Selecting the right Architect Professional Liability Insurance policy involves heedful circumstance of several factors. Here are some steps to aid architects make an inform determination:

- Assess Your Needs: Evaluate the specific risks associate with your practice, including the types of projects you undertake and your claims history.

- Compare Policies: Obtain quotes from multiple insurers and compare the coverage, limits, deductibles, and premiums.

- Review Policy Terms: Carefully read the policy terms and conditions to see you interpret what is covered and what is excluded.

- Consult with a Broker: Working with an insurance broker who specializes in Architect Professional Liability Insurance can cater worthful insights and help you notice the best policy for your needs.

Note: It is crucial to review your policy annually to ensure it continues to meet your needs as your practice evolves.

Common Exclusions

While Architect Professional Liability Insurance provides comprehensive coverage, there are certain exclusions that architects should be aware of. Common exclusions include:

- Intentional Acts: The policy does not cover claims originate from intentional or criminal acts.

- Contractual Liability: Claims resulting from contractual obligations that are not related to professional services may be excluded.

- Pollution Liability: Coverage for claims related to environmental pollution or wild materials may require additional endorsements.

- Employee Dishonesty: Claims rise from the dishonest acts of employees are typically excluded and may demand separate coverage.

Best Practices for Risk Management

besides get Architect Professional Liability Insurance, architects can enforce respective best practices to manage risks and trim the likelihood of claims:

- Thorough Documentation: Maintain detail records of all project communications, decisions, and changes to ensure transparency and answerability.

- Regular Training: Provide ongoing training for staff on best practices, industry standards, and risk management strategies.

- Quality Control: Implement full-bodied caliber control processes to place and address possible issues early in the project lifecycle.

- Clear Communication: Establish clear lines of communication with clients, contractors, and other stakeholders to care expectations and resolve issues promptly.

Note: Regularly review and update your risk management strategies can aid ensure they remain efficient as your practice grows and changes.

Case Studies: Real World Examples

To illustrate the importance of Architect Professional Liability Insurance, consider the postdate case studies:

| Case Study | Scenario | Outcome |

|---|---|---|

| Design Flaw | An architect's design for a commercial building resulted in structural issues, star to significant repairs and delays. | The architect's Architect Professional Liability Insurance covered the sound defense costs and settlement, protecting the architect's fiscal assets. |

| Construction Delay | A task was delayed due to errors in the architect's drawings, ensue in extra costs for the client. | The indemnity policy covered the claim, allowing the architect to continue their practice without financial disruption. |

| Project Management Failure | Ineffective projection management led to cost overruns and client dissatisfaction, result in a claim against the architect. | The insurance furnish coverage for the sound defense and settlement, helping the architect maintain their reputation. |

Conclusion

Architect Professional Liability Insurance is an essential component of risk management for architects. It provides fiscal security, enhances report, and offers peace of mind, permit architects to focus on their work without the constant worry of potential claims. By understanding the types of coverage, factors affect premiums, and best practices for risk management, architects can get inform decisions to protect their practice and check long term success. Regularly reviewing and update policy policies and risk management strategies is essential to adjust to the evolving needs of the practice and maintain comprehensive protection.

Related Terms:

- establish designer professional indemnity indemnity

- architectural professional liability indemnity

- professional engineer liability insurance

- architects and engineers professional liability

- policy for architects and engineers

- professional liability for architects